We all do it. Consciously or not, we all lie to ourselves and it costs us money.

“The majority of your beliefs, particularly in business, are driven by what you want to be true.” -Tom Asacker, author of The Business of Belief

We form beliefs about things based on experiences and perceptions that are often just fragments of reality. An initial impression or a bit of passed down wisdom that we’ve heard from a young age can have an enormous and long-lasting effect on our expectation of how things are supposed to work. This leads us to mainly see only what we already believe and discount things that challenge those beliefs. It’s called confirmation bias and it’s probably costing you money right now.

For example, let’s say you’re a typical investor with a typical 60/40 type of account split between stocks and bonds. The vast majority of your stock exposure is likely to be in U.S. equities. You’re feeling pretty good right now. Despite what happened back in 2008, recent performance has confirmed what you probably suspected to be true – there’s no better place to be over the long haul than the market. No need to get complicated or fiddle around with other types of securities or markets or strategies.

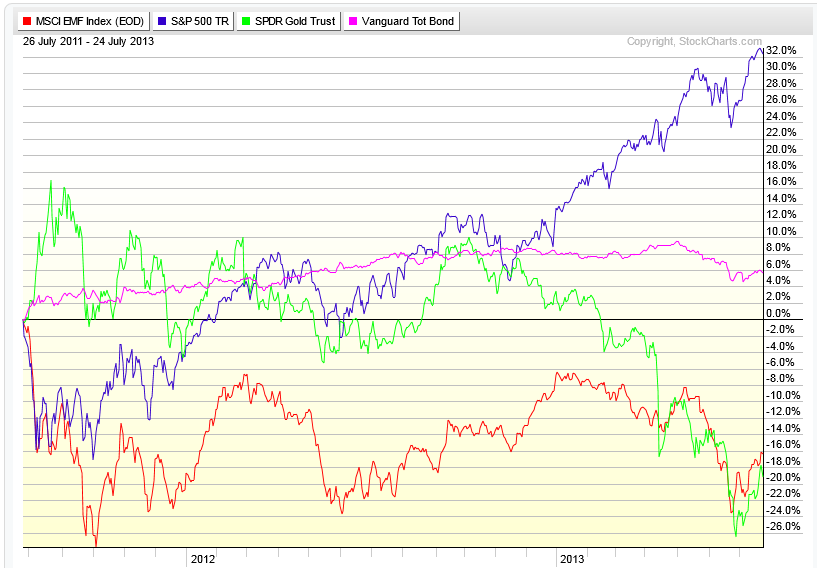

Here’s the last couple of years of US Stocks (blue line) compared to Bonds (pink line), Emerging Markets Stocks (red line) and Gold (green line):

It’s been a shellacking. Domestic stocks have been great, everything else has been ugly. So, if you have an account that is dominated by US stocks, there’s a good chance that recent performance has confirmed your pre-existing belief.

It’s been a shellacking. Domestic stocks have been great, everything else has been ugly. So, if you have an account that is dominated by US stocks, there’s a good chance that recent performance has confirmed your pre-existing belief.

But what about those times when reality doesn’t follow the script?

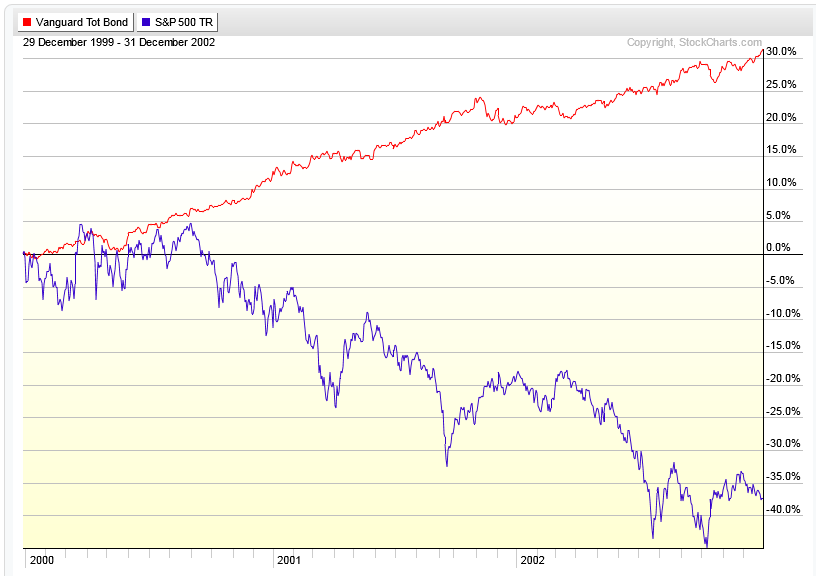

This was a three year period where bonds massacred stocks. Experience and perception at the time was leading people to sit in my office and say things like, “why in the world would I ever own stocks again when I can take less risk with bonds and make a lot more money?”

This was a three year period where bonds massacred stocks. Experience and perception at the time was leading people to sit in my office and say things like, “why in the world would I ever own stocks again when I can take less risk with bonds and make a lot more money?”

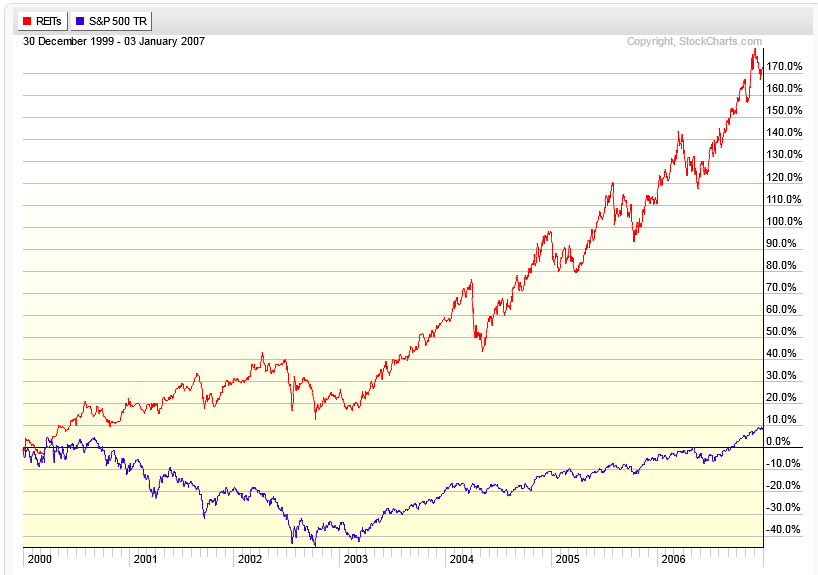

Remember real estate?

Here were seven years in a row where REITs pummeled the market. If experience and perception form beliefs, then this is a perfectly rational explanation for why there were a couple dozen house flipping shows on TV back then. Our experience, for the better part of a decade, was that investing in stocks was futile in comparison to real estate speculation.

Here were seven years in a row where REITs pummeled the market. If experience and perception form beliefs, then this is a perfectly rational explanation for why there were a couple dozen house flipping shows on TV back then. Our experience, for the better part of a decade, was that investing in stocks was futile in comparison to real estate speculation.

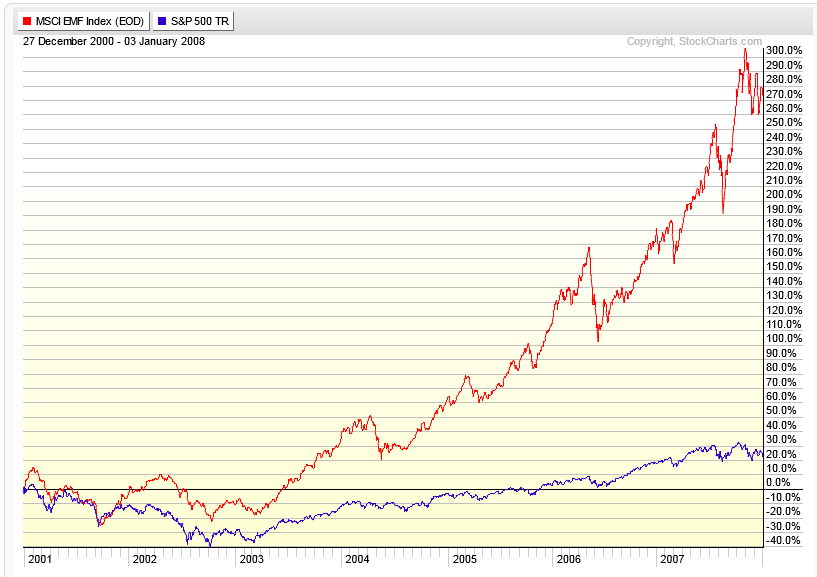

Do you know any “gold bugs” who believe that putting money in anything but gold is hopelessly naive?

Their belief was absolutely confirmed by this six year period. Adjusted for inflation, this is six years where stocks returned nothing while gold skyrocketed. Reality or fragment of reality?

Their belief was absolutely confirmed by this six year period. Adjusted for inflation, this is six years where stocks returned nothing while gold skyrocketed. Reality or fragment of reality?

Finally, here’s a look at Emerging Markets vs. the US:

If the last two years tells us something about the smartest way to invest, what do these seven years tell us?

If the last two years tells us something about the smartest way to invest, what do these seven years tell us?

At this point, the typical person with a pre-existing bias toward the typical 60/40 buy & hold approach might be thinking something like, “cherry picking two or three or six or seven year periods doesn’t prove anything – I’m interested in the long term.”

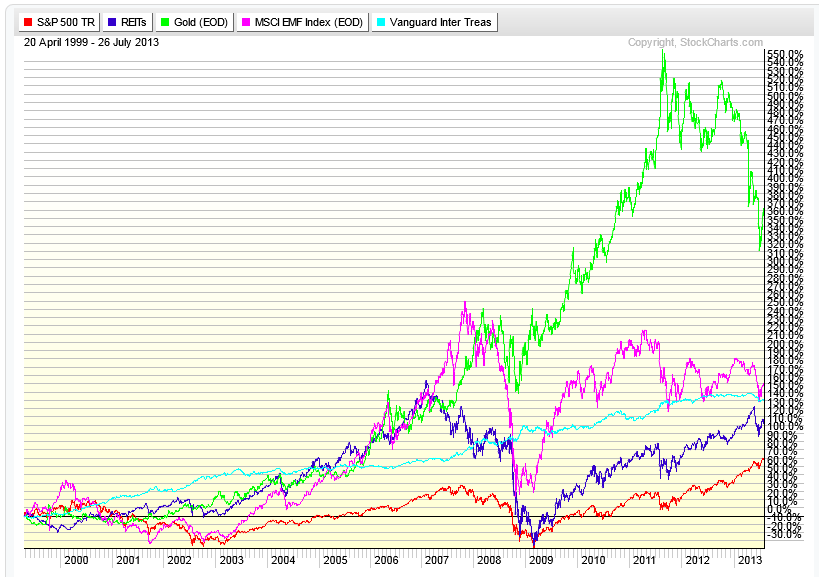

This chart will only let me go back fourteen years with all five classes – US Stocks (red line), Real Estate (blue line), Bonds (aqua line), Emerging Markets (pink line) and Gold (green line).

Over the last fourteen years, US Stocks were the worst performing of all five classes. By a longshot. This is another fragment of reality, but one that makes an interesting point. Try to answer the following questions as objectively as possible:

Over the last fourteen years, US Stocks were the worst performing of all five classes. By a longshot. This is another fragment of reality, but one that makes an interesting point. Try to answer the following questions as objectively as possible:

- Is it reasonable to assume that investments other than US Stocks have the potential to outperform stocks in any given year?

- Is it reasonable to assume that this potential outperformance could be significant?

- Is it reasonable to assume that this outperformance could potentially be sustained for a long period of time?

- Is it possible for us to know in advance when these periods of potential outperformance will begin, how long they will last, and the magnitude of the difference?

So that’s three yes answers and a no. The typical approach can work, but knowing that it will always be the best, most reasonable way to invest for the long haul could be costing you a literal fortune. The hard part for most people is that challenging a long-held belief takes a lot of effort and our brains are wired to avoid effort whenever possible. Challenges usually get put off until our hand is forced by some type of unbearable pain.

If you are interested in challenging beliefs without having to endure unbearable pain, here are some thoughts to keep in mind:

- Your investing life is relatively short. Market performance can vary wildly from decade to decade and from country to country. Planning for outcomes based on the market’s 100 year average return is just as pointless as basing it on two years of performance. Past performance of any length is not a reliable guide to your future.

- Think about the future not as an average number, but as a range. A reasonable plan has to account for a spectrum of possible outcomes. It has to protect you from disaster and allow you to grasp opportunities when they present themselves.

- All investment strategies ebb and flow. They all have certain conditions that are favorable and others that are more challenging. The hard part can be distinguishing the difference between a normal down part of a cycle and something that needs fixing. You should be able to define, in advance, how to tell them apart.

- Discipline is required for any strategy to work. Discipline requires confidence. Confidence requires knowledge and realistic expectations. If you have doubts or discomfort, ask questions – find answers.

Enjoy this post? Interested in original investment ideas? Please subscribe now to be notified whenever a new article or free white paper is published.

Disclaimer: Past performance is not indicative of future returns. Information displayed is taken from sources believed to be reliable but cannot be guaranteed. All indices are unmanaged and investors cannot invest directly into an index. Ideas and opinions expressed in this article are the sole responsibility of Patrick Crook/PLC Asset Management and do not reflect any stated opinions of Commonwealth Financial Network, National Financial Services LLC or any other person or entity.